FXTM Daily Market Analysis - Business (2) - Nairaland

Nairaland Forum / Nairaland / General / Business / FXTM Daily Market Analysis (3317 Views)

FXTM Is A Scam. Trade With Them At Your Own Risk (2) (3) (4)

| Re: FXTM Daily Market Analysis by Forextime: 5:31am On Sep 06, 2017 |

Daily Fundamental ForexTime ( FXTM ) US woes cause dollar bears to strike  It's been a perfect storm for the USD bears today as the USD plummeted against major pairs and commodities. For some time the USD has been quite weak and major pairs have capitalised on it when possible, however there has been a major weather event recently with Hurricane Harvey causing major flooding and causing a large amount of damage, and also another storm likely to hit and impact Florida. Couple to this the huge backlog of political work that needs to be done by the end of the month and you can see why markets are not happy with the current US situation. The major bearish sign though was the durable goods orders m/m which fell to -6.8% (-2.9% exp) which gave the dollar bears another chance to dump the USD.  No where was this felt more than the commodity currencies which surged higher on the back of the USD weakness. After recent bearish behaviour after the last few months the NZDUSD has surged higher today on the back of the weaker USD, and also positive Australian outlook from the Reserve Bank of Australia. The push upwards today was very strong and cracked through the trend line before hitting resistance around the 20 day moving average. The bears have since pushed it back down but the new daily candle is searching to find weakness and it may find it with the current weak USD. I'm not sure how much further it can however rise, but resistance at 0.7323 and 0.7400 are likely to be strong targets for traders in the market. If we do see a fall back down the charts and the trend continuing then I would expect to see support at 0.7219 and 0.7157 be the focus. Oil has surged today on the back of a number of key things. Firstly there are talks that Saudi Arabia and Russia are looking to extend further rate cuts. Additionally, the USD has been somewhat weaker and this always leads to a rise in the value of oil in the short term. Further adding to this is the fact that refineries in the US are starting to come back into full swing, and there demand for oil products will increase to make up for lost ground - if they're not already at full capacity. US oil inventory data would normally be the next thing also to focus on for oil traders but due to the US public holiday it's going to be a day later than normal.  Technical traders will be focused on the failure of oil to break through resistance today at 48.82. For some time now there has been a bearish expectation for the market and it had been trending lower, but the last few days have seen jumps and expectations are the bulls might be looking to take control again. Certainly oil is big on trending, but each wave has been weaker. If the market fails to break and hold above 48.82 then I would expect it to swing lower to 46.50 and 45.47.  |

| Re: FXTM Daily Market Analysis by Forextime: 6:07am On Sep 12, 2017 |

Daily Fundamental ForexTime ( FXTM ) USD beats monday blues  The dollar has begun a strong rally on the charts and US markets are surprisingly upbeat, most likely on the bipartisan actions that have occurred in the US, with Trump working with the democrats to push through debt ceiling reform and provide aid for Harvey and Hurricane Irma as it hits Florida. This US resolve has been somewhat missing over the previous month, with many struggles and failures for the Trump administration as well as added heat from the investigation into Russia and its influence in the recent US elections. Some economic information also had a boost with consumer credit lifting positively to 18.5B (15B exp) showing that the consumption based economy which is the United States is still going ahead full steam and there may be plenty more left in the tank. With all the turmoil recently for the USD the one winner may in fact be the S&P 500, which has been lifting on speculation that the FED will not lift interest rates in December as many had been expecting. The mindset is that the hurricanes will have an impact on the economy, and force the FED to act more dovish in the later part of the year. So with the FED being dovish the S&P 500 is looking to close at record highs and the market is poised to continue its bullish run against all odds.  With the S&P climbing through resistance at 2484 and closing above the market is looking quite bullish an extension up to the magic 2500 mark looks on the cards. Anything above the 2500 mark would most likely be aiming for the next psychological level at 2524. In the event we did see a strong pull back on the chart my focus would be on 2484 and 2459 with the 100 day moving average being the real test if the markets start to become bearish. The other key pair which has certainly been in the headlights today has been the cable which saw some stiff resistance at 1.3224. Now the UK economy has been undergoing a tough time with the uncertainty around Brexit and this has not been helped by comments from the Euro-zone which have tried to undermine the position of the British. But for the most part it has been dollar weakness which has enable the pound to climb so high. A reversal of this position could certainly be in the works after failing to climb any higher at 1.3224.  Expectations are now building that we could see the bears taken a decent swipe as the market swings lower. I would certainly be aware of the 20 day moving average which does have a habit of providing support. Traders are likely to target the key area of 1.3000 which is a psychological level, but also a strong area of support and could be the land in the sand for the bulls to look to regain control - it certainly has a lot to play for around this level given the recent history.  |

| Re: FXTM Daily Market Analysis by Forextime: 5:42am On Sep 14, 2017 |

Daily Fundamental ForexTime ( FXTM ) Global tensions set to boost metals  North Korea is on the move again when it comes to upsetting the western world, as reports are now surfacing that they will test launch another ICBM and potentially point it towards pacific targets. With the latest rounds of sanctions having little to no effect, it seems likely that the US may rattle its sabre once more at North Korea with further tough talk, this could in turn have a flow on effect in the markets which will look to hedge on any escalation risk. Albeit at the last possible moment if traders can help it, but so far the bounce off these events has been substantial. One of the key winners of such trades is indeed precious metals, which speculators enjoy to the fullest when it comes to hedging against risk. While traditionally a hedge against inflation, it has since become the go to move for traders look to hedge against political events as well.  Silver for me is the key metal I will be watching for a number of reasons. Firstly it's a little more robust technically than gold, and secondly it seems to be less likely to spike wildly on big movements but instead take a direction and go with it. Also for silver traders support was recently tested at 17.696 and the market quickly pushed back on the occasion. So far the bulls are trying to hold and are holding out on a weaker USD and further political upheaval. In the event it does slide further the next level can be found at around 17.352, however, the 20 day moving average should also be treated as dynamic support in this instance as well. On the upside it's clear to see that resistance can be found at 18.214 and 18.607, beyond these levels might be quite hard as silver does start to struggle above the 20 dollar mark, but any massive unrest could certainly send it flying higher. If you're looking for further excitement in your trading day then the Australian dollar is set to swing low or high depending on your views of the current employment data due out shortly. The Australian labour market has been full of surprises recently, and many Australians are expecting the Reserve Bank of Australia to perk up more if the labour market continues to expand at the present pace. Today's reading is expected to come in at 20K, but the previous reading of 27.9K is what the market may be hungering for here. Certainly any movements in the participation rate will also be closely watched as well.  At present the AUDUSD has slipped back under the 80 cent market and is trending lower on the stronger USD. Resistance can be found at 0.8000 and 0.8110 with the 80 cent market likely to break on positive employment data. In the event we see weaker than expected data then I would expect the AUD to plunge sharply down to support at 0.7901 and potentially 0.7821 in the coming weeks. |

| Re: FXTM Daily Market Analysis by joelreg(m): 7:31pm On Sep 28, 2017 |

who still uses forextime having a bad time with them I made a deposit to the bank they provided EXPOBANK more than 5 business working days they stipulated yet my trading account is yet to be credited. the funny part they removed the bank from my funding page option Each time I chatted with them they kept telling me repetitive stuff. |

| Re: FXTM Daily Market Analysis by save4live: 12:55pm On Dec 12, 2017 |

Whether you are looking to buy and resell gold and silver or looking to diversify your portfolio then this is the place for you. At MintBuilder you can buy physical gold and silver at very competitive rates using different payment options. As an example, at the time of writing this, MintBuilder's 2.5g gold bars were ~$50 cheaper than the same product on Amazon! Alternatively, you can also join up with a MintBuilder wholesale team and start to earn commissions paid in either gold, silver, cash or ...! These commissions range from $250-$10,000 a week! That's not a typo, $10,000 a week! Click here for more http://www.MintBuilder.com/266254. If you like what you see but are worried about how to go about it, check out this youtube channel https://www.youtube.com/watch?v=C_W8fif2yC0&feature=em-uploademail. You can contact me for more information. Whatsapp +2348186540455 Cheers! |

| Re: FXTM Daily Market Analysis by Forextime: 5:03am On Jul 20, 2018 |

Daily Fundamental ForexTime ( FXTM ) EM Currencies slide as Dollar appreciates  Emerging market currencies have been treated without mercy by a broadly stronger Dollar, yet again. The Dollar Index appreciated to its highest level this year above 95.50 due to heightened expectations over higher US interest rates this year. The Chinese Yuan, Malaysian Ringgit, Indonesian Rupiah, Singapore Dollar and most other major EM currencies have all felt the heat. With Dollar strength likely to remain a dominant market theme and global trade tensions negatively impacting risk sentiment, EM currencies appear destined for further punishment. In regards to the Chinese Yuan, price action continues to suggest that the local currency remains heavily influenced by external forces. With the Yuan already weakening to a fresh yearly low, further losses could be expected amid an appreciating Dollar. Taking a look at the USDCNY, a decisive daily close above 6.750 could inspire an incline to levels not seen since June 2017 around 6.810 Dollar bulls are back in town It has certainly been an incredibly positive trading week for the Dollar. Federal Reserve Chairman Jerome Powell’s bullish testimony could be one of the primary drivers behind the Dollar’s appreciation, especially when considering how he reinforced expectations of higher US rates this year. Taking a look at the technical picture, the Dollar Index has scope to venture towards 96.00 and 96.40 if bulls are able to secure a daily close above 95.00. Commodity spotlight – Gold Gold is poised to conclude this week in heavy losses thanks to an appreciating US Dollar. The yellow metal remains under intense pressure on the daily charts with prices trading marginally below $1220 as of writing. With the combination of Dollar strength and prospects of higher US interest rates eroding appetite for the zero-yielding metal, Gold is firmly bearish. Sustained weakness below $1200 could inspire a decline towards $1209 and $1200, respectably. |

| Re: FXTM Daily Market Analysis by Forextime: 8:52am On Jul 31, 2018 |

Daily Fundamental ForexTime ( FXTM ) Bank of Japan unwilling to shift gears yet  After weeks of speculation that the Bank of Japan may begin to adjust its stimulus program, the central bank once again decided not to join the global trend towards tighter policies. The BoJ left its overnight interest rates unchanged at -0.1% and reiterated that it would resume buying Japanese Government Bonds to keep the 10-year yields around 0%. The bank may allow for more flexible movement on the 10-year bonds, however this isn’t considered a significant shift in policy. The BoJ also made tweaks to its ETF purchases, as it increased the composition of TOPIX-linked ETFs while shifting slightly away from the Nikkei 225 Index, but maintained its annual pace of ETF buying. It seems the Bank of Japan will be the last major central bank to pull the trigger on tightening policy as the Japanese economy continues to struggle with stubbornly low inflation levels. This should allow further widening in spreads between Japan’s bonds and other global bonds towards year-end, suggesting that the Yen is likely to remain under pressure for the near future. The Federal Reserve is next in line to announce policy on Wednesday. That’s why today’s Core Personal Expenditure figures carry significant importance. If Core PCE came in at 2% or above, it would reinforce expectations for two more rates hikes in 2018. Many traders want to know whether President Donald Trump’s criticism of the Fed will lead to a change in language; I believe there will be no change in guidance and the Fed will continue sending the message that more rate hikes are on the way. We also have inflation and Q2 GDP numbers from the Eurozone. Consumer Price Index figures are expected to rise 2.0% y-o-y in July, remaining unchanged from June. Meanwhile, GDP growth is expected to see a 0.3% fall from a year ago, towards 2.2%. In equity markets, the tech sector continued to weigh on sentiment. Shares of Facebook, Twitter and Netflix plunged further on Monday, as investors started to become more worried about their business models after they announced their latest earnings results. Amazon and Alphabet were also dumped. Meanwhile, all eyes will shift to Apple earnings today in the hopes of providing some support for FAANG stocks. |

| Re: FXTM Daily Market Analysis by Forextime: 5:29am On Aug 03, 2018 |

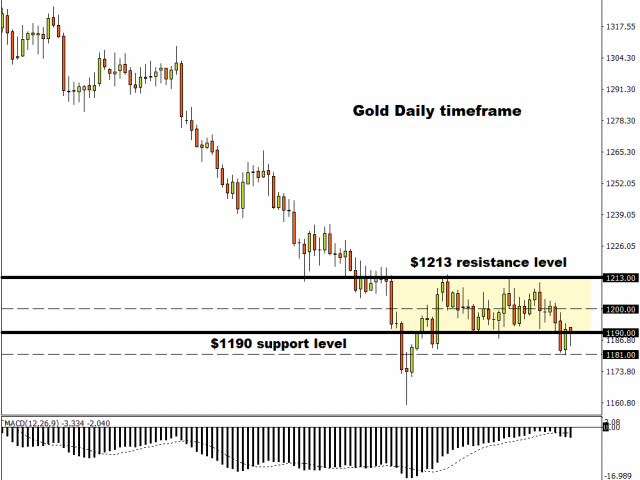

Daily Fundamental ForexTime ( FXTM ) Gold slips ahead of non-farm  The US labour market has continued to impress as of late as US initial jobless claims came in strong at 218K (220K exp), showcasing the labour market surging ahead. However US durable goods orders continued to be less upbeat than expected coming in at 0.2% m/m (0.5% exp), this is not likely to be a big mover for the USD however as the labour market continues to be the key FOMC focus as well as inflation additionally. With all this in mind it looks likely that interest rates will continue to rise, and coupled with the USD flight we've seen lately that the USD will continue to be the dominate currency in financial markets at present. One of the key movers as outlined yesterday has been of course gold, which has been suffering for some time now. So far today we've seen a very strong break through support at 1213 as gold looks to push down to the psychological level at 1200. I feel this is not likely to hold given the current market sentiment and a more realistic target may be support at 1189, which has been a long term support level in the past. If gold did reverse then resistance levels at 1240 and 1258 would be key targets for traders in this market. However, I feel the 20 day moving average is likely to be the main level of dynamic resistance in this market at present, given how badly gold bugs are feeling at present. The other big loser at present in the markets has been of course the Australian dollar which finds itself under pressure constantly. The services index was released today and showed a sharp decline to 53.6 - still showing expansion, but not anywhere near the previous reading of 63. Markets when focusing on the AUDUSD will now be clearly focused on non-farm payroll figures due out tomorrow which could add further pressure to the AUDUSD which has been bearish for some time now. I'm apprehensive about any bullish movements in the current market, as the USD continues to strengthen. On the charts the AUDUSD has continued to be bearish and shows no sign of letting up. We've so far seen sharp falls and support at 0.7310 is looking to be the next major target. On the flip side, if the AUDUSD was to rise it would find strong resistance at 0.7377 and with the 50 day moving average as well - with a potential trend line in play as well, but we've not seen any real tests on this level. All in all though, it feels like the AUDUSD is likely to spiral further lower. |

| Re: FXTM Daily Market Analysis by Forextime: 9:27am On Aug 06, 2018 |

Daily Fundamental ForexTime ( FXTM ) Is Trump truly winning the trade war?  Escalating trade tensions between the U.S. and China remain the financial markets’ hottest topic. President Trump seems to be celebrating winning the first battle of this war, saying that “tariffs are working big time” in a Tweet on Sunday. He believes that they will enable the U.S. to start reducing the large amount of debt accumulated throughout Obama’s administration. Trump also cited that the steep fall in Chinese equities as evidence that tariffs are working. In his opinion, they will make the U.S. much richer than it currently is and that “only fools would disagree”. The tariffs so far are approximately on $85 billion of imported goods. Assuming a 25% tariff, it would raise $21.25 billion. This number represents 1.33 % of the $1.6 trillion in additional debt President Trump has accumulated since taking office in 2017 and only 0.1% of the current $21 trillion in total debt. So, it doesn’t seem the imposed tariffs would reduce the American debt substantially. In my opinion, a large portion of the tariffs will be paid by U.S. consumers and I also expect CPI figures to begin reflecting these higher prices, especially if Trump’s administration imposes additional tariffs on $200 billion of Chinese goods. Rising inflation leads to higher U.S. interest rates, translating into higher cost of borrowing and debt servicing. Several U.S. companies have cut their profit forecast as a result of these tariffs, especially car makers; shares of GM, Ford, and Fiat Chrysler fell sharply after announcing their results. Other U.S. companies affected by Trump’s global trade war include Tyson Foods, Harley Davidson, United Technologies, Caterpillar and Coca-Cola, among several others. This explains why the S&P 500 failed to reach a new record high, despite 81% of companies so far managing to beat their profit forecast in one of the best earning seasons in history. Given that we’re almost at the end of earning season, trade wars will return to dominate the headlines. The next big risk is likely to be the U.S. midterm elections in November. I think there’s a high chance that the Democratic Party will take over the U.S. Congress and end the Republican single-party control. This won’t be good news for equities, and I expect to see rotation to non-cyclical stocks and an increase of cash in investors’ portfolios. |

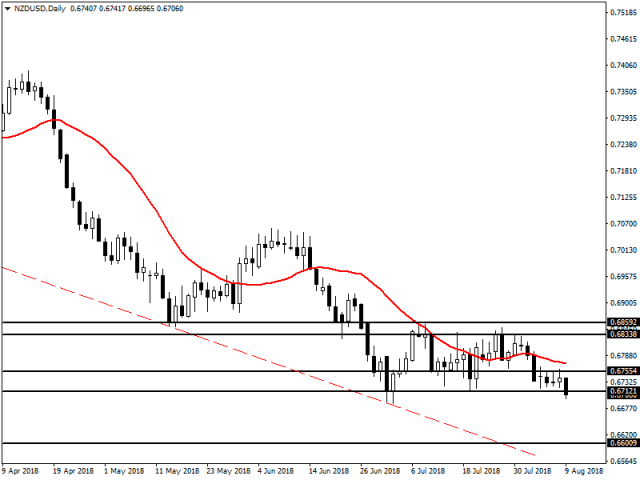

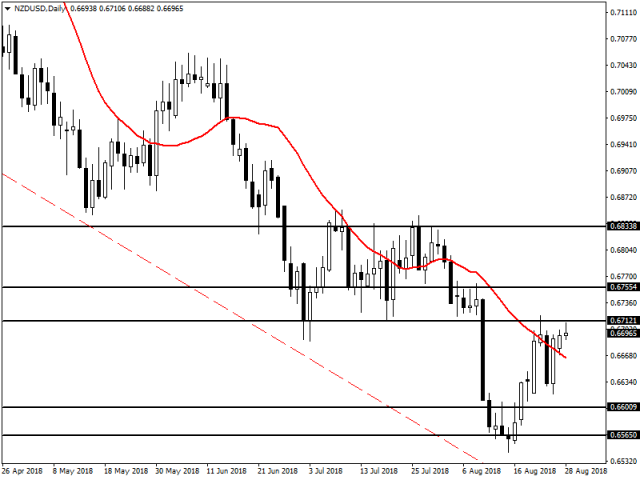

| Re: FXTM Daily Market Analysis by Forextime: 5:32am On Aug 09, 2018 |

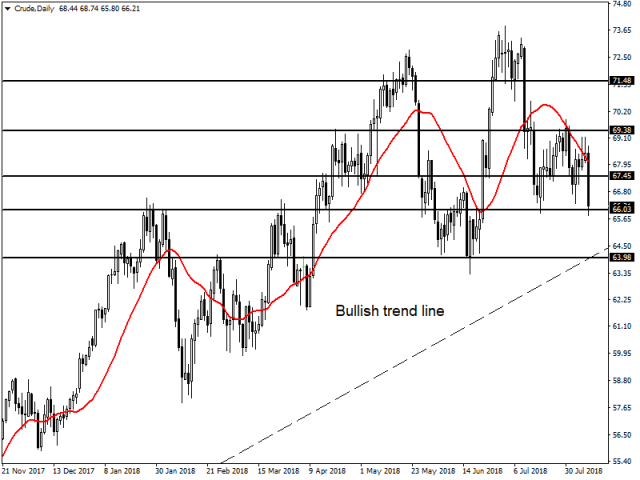

[b]Daily Fundamental ForexTime ( FXTM ) NZD falls on RBNZ dovish stance[/b  It's been an exciting morning for the Reserve Bank of New Zealand as they announced that they see rates being held at 1.75% until 2020 in the current market environment . This pails in regards to previous assumptions from economists that we would see a rate rise in early 2019, and with that thrown out of the window the NZD has fallen accordingly. There is hope that the NZ economy will see moderate growth to say the least, and that core inflation will also pick up in the long run, however all things considered and a trade war going on, it may be a hard ask to say the least. One thing is very clear though, and that is the RBNZ has taken a very dovish stance and provided some stern guidance on expectations and as a result markets will be looking to price this in.  For the NZDUSD it has been a case of free fall at this stage with the NZDUSD crashing through support at 0.6712 and heading down towards support at 0.6600. Certainly this is what the RBNZ is hoping for as a weaker kiwi dollar leads to higher export prices for producers. If the NZDUSD is able to swing things around and actually be bullish then resistance at 0.6755 is likely to be the main focus, with the 20 day moving average hovering around there. Beyond this there is a strong resistance band at 0.6833 and 0.6859 which will likely contain any bullish ambition. All in all though, it's likely the bears that will remain in control on the back of all this news. The other big mover today has been oil as it shot down the charts on some bearish swings. The catalyst of course was oil inventory data which showed a weaker than expected drawdown of -1.35M barrels (-3M exp) and a surge in gasoline inventories as well to 2.9M (-1.9M exp). All of this has taken the heat of the oil market which had been looking stronger on the back of Iran sanctions.  Looking at the movements of oil on the charts, it's clear to see that it has shot down lower and hit support around 66.03 in this instance, before seeing a small retreat. If we continue to see bearish pressure here then I would expect a fall to 63.98, but more importantly there is the trend line which could create an even bigger hurdle given it's bullish. If the bulls are able to come back in then resistance at 67.45 and 69.38 are likely to be the key targets, with the market seemingly being a little unsure on oil being over 70 dollars a barrel. |

| Re: FXTM Daily Market Analysis by Forextime: 3:55am On Aug 16, 2018 |

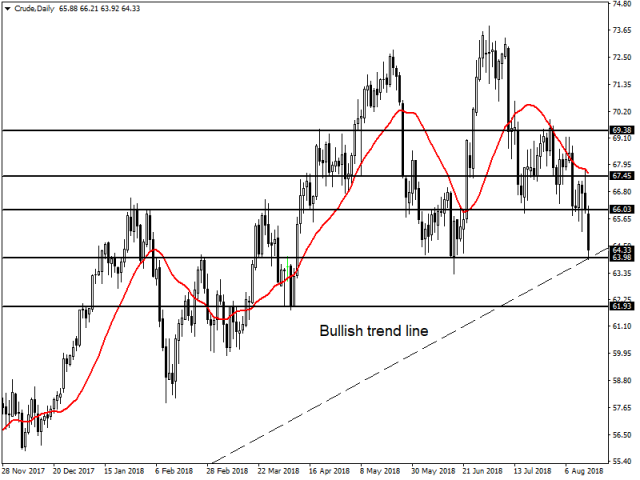

Daily Fundamental ForexTime ( FXTM ) NZD falls on RBNZ dovish stance  USD bulls have continued their strong run globally, as weakness in overseas market continues, but also strong economic growth continues to be a major factor. US retail sales m/m were very strong today coming in at 0.5% (0.1% exp), showcasing that consumers are not worried about tariffs or the high USD for that matter and currently are out spending. If consumption is a good indicator of economic health it may also bolster inflation expectations as retailers feel they can increase prices slightly during periods of expansion without fear of losing to many customers. So while economic growth is strong so far the markets will be looking to the FED to see if it changes its mind about anything and if more future rate hikes are coming in the long term. On the markets though today oil was for me one of the more interesting trades as it hit the bullish trend line and beat a retreat shortly after. US oil inventories once again showed much more stronger figures than anyone expected with a surplus of 6.8M (-2.5M exp), with only gasoline registering a drawdown on stockpiles. Oil has also struggled against a robust USD at present which has managed to hold back the oil bulls as well, but with OPEC holding back supply it's likely we could see prices remain elevated.  Looking at oil on the chart we've hit the sweet spot for bullish support here with the trend line coming into play and also support at 63.98. Technically I would expect the bulls to be stronger here as the market has a chance to push back against the recent trend, however at present it's still looking a bit weak. With that weakness in mind I would be careful of a push through here to support at 61.93; if we did see that happen then the bears are likely to really take hold of things in the current market climate. If the bulls do however wrestle back control resistance can be found at 66.03 and 67.45. The pound has continued to come under large pressure from markets as the Brexit debate continues to rage and the prospect of a hard Brexit looks to impact markets. I would expect more impactful debate on Brexit from the UK government after the summer break, nevertheless the major sticking points have no solutions and it looks like it could get drawn out for much longer than anyone expected and markets won't be loving it.  For the GBPUSD the fall is likely to continue with the uncertainty and support at 1.2652 has so far stopped any further movements lower. If we a see a breakthrough at this level then I would expect to see it fall as low as 1.2461 and even potentially further lower if markets feel a no deal Brexit is coming. On the flip side, if the bulls can push back then resistance can be found at 1.2798 and 1.2958 as well. |

| Re: FXTM Daily Market Analysis by Forextime: 11:13am On Aug 24, 2018 |

Daily Fundamental ForexTime ( FXTM ) Quiet market before Powell Jackson Hole speech  There is a lower level of market volatility at the end of the week, with investors on stand-by mode before Federal Reserve Chair Jerome Powell speaks at Jackson Hole later today. Traders are probably on the edge of their seats wondering whether Powell will respond at all to the criticism from President Trump towards US interest rate policy earlier in the week, but the most market-friendly way to respond to such comments would be to ignore them. The Federal Reserve does remain set on raising US interest rates once again next month, and there is no reason for the Fed to deter from this path. I personally doubt that he would acknowledge the comments made by President Trump during Jackson Hole. Powell might be able to create some volatility for traders is if he highlights the potential impact the ongoing trade tensions is a risk to the global economy. There are indications that the global economic outlook is slowing when compared to this time last year, and the latest FOMC Minutes release from this week did create a picture that Federal Reserve policymakers are concerned about the prolonged trade tensions. If Powell suggests that these concerns over trade tensions could also weaken the US economic outlook, this would represent a risk for the Dollar. Elsewhere a threat for financial market volatility would be if Jerome Powell takes an unexpected turn towards offering monetary guidance on what the outlook for 2019 could bring. The market is already pretty much set-on for the Federal Reserve to raise US interest rates next month with the door also remaining open for a potential US interest rate increase before the year concludes, but there isn’t much guidance on what to expect next year. It might be a little premature at this stage to speculate, but if Powell suggested that 2019 would bring a less active approach towards raising US interest rates this would be seen as a negative for the US Dollar. |

| Re: FXTM Daily Market Analysis by Forextime: 4:29am On Aug 28, 2018 |

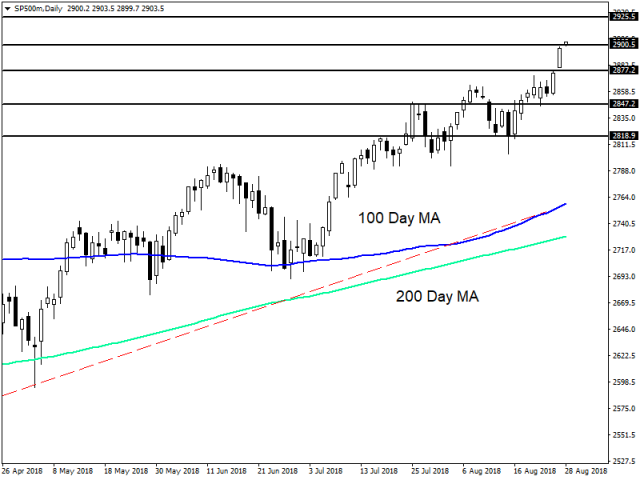

Daily Fundamental ForexTime ( FXTM ) Global risk appetite increases on US and Mexico deal  It has been an incredibly bullish day for the US markets after the US and Mexico agreed in principal on a trade deal to replace NAFTA. While Mexico has agreed in principal around this deal the main issue for many has been the exclusion of Canada thus far, with a separate agreement looking to be reached in the long run for Canada and the US and Mexico. This move however will need approval by congress and the senate but markets believe it will happen and as a result and we've seen some very bullish moves at the start of the week globally.  Looking at the S&P 500 it is clear that investors thus far believe that any trade deal that has been agreed will favour the US economy heavily, as Trump has been a staunch opponent of the current NAFTA deal and the effect it had on blue collar workers. While protectionism of certain industries is not ideal in any situation the equity markets believe that in this case it may be warranted and have pushed the market to a record high of 2900. With this being a key level of resistance for the market we're waiting to see if the market has further legs and can lift to 2925 at present. In the event that it does not have the movement that was envisioned then a potential fall back to support at 2877 could likely be on the cards. With further falls in the long run to 2847 and 2818. However, the US equity markets continue to be upbeat so I am looking at this as very bullish in the long run. One of the other moves at the start of the week and one to watch has been the New Zealand dollar which has crept up the charts thus far. Markets I feel have not been expecting this one, but some recent weakness in the USD has given it a bit of a reprieve and we've seen some small gains. In the long run though, the New Zealand economy is still suffering and it may be a very long time until we see any sort of rate rises in the current market environment.  Looking at the NZDUSD on the charts it has been quite the aggressive mover as of late and the bears have taken a big chunk out of it. Resistance at 0.6712 has so far held back any bullish movements as I feel markets are cautious over any rises. However, there is further potential to rise to 0.6755 and 0.6833 in the long run if bullish sentiment continues. If the bears take back control then support levels can be found at 0.6600 and 0.6560 at present. |

| Re: FXTM Daily Market Analysis by Forextime: 10:27am On Sep 05, 2018 |

Daily Fundamental ForexTime ( FXTM ) BoE inflation report hearings in focus, Dollar powers higher A sense of gloom was evident across financial markets today as worries over rising trade tensions and emerging market weakness weighed heavily on global sentiment. Looming U.S. tariffs set to be imposed on $200 billion worth of Chinese goods as soon as Thursday brings on oppressive feelings, while uncertainty over NAFTA negotiations has compounded anxieties. Caution can be reflected across global equity markets, with Asian stocks concluding mixed while European shares struggle for direction. Emerging market currencies witnessed further weakness on global trade tensions and Dollar strength. No prisoners were taken as the Turkish Lira, Argentina Peso, South African Rand and many other EM currencies felt the burn. The outlook for EM currencies remains gloomy, especially when considering the turmoil in Turkey and Argentina, trade war fears and prospects of higher US interest rates all present downside risks ahead. The British Pound had a rocky start to the week after Brexit negotiator Michel Barnier warned that he “strongly” disagreed with key sections of Theresa May’s Brexit proposal. Sellers attacked the Pound further this morning on reports that UK construction activity slowed in August. Much attention will be directed towards the UK’s inflation report hearings where Mark Carney and several MPC members are set to testify before parliament. Investors will be paying very close attention to any comments around monetary policy, economic outlook and ongoing Brexit developments. Will he stay or will he go? This remains a recurrent question on the mind of many investors. Lawmakers are likely to use this opportunity to quiz Carney about his future plans. The battered Pound could receive a knock out blow if Carney strikes a dovish tone and talks down rate hike prospects. In the currency markets, the Dollar was King as concerns over escalating US-China trade tensions boosted safe-haven demand for the currency. Another key driver behind the Greenback’s healthy appreciation is speculation over higher US interest rates this year. Taking a peek at the technical picture, the Dollar Index punched above the 95.50 level. A solid daily close above this region could inspire a move towards 95.80. Gold bears were back in action on Tuesday thanks to a broadly stronger US Dollar. With the mighty Dollar set to dim Gold’s shine and US rate hike expectations denting appetite for the zero-yielding metal further, the outlook remains tilted to the downside. Sustained weakness below the $1,200 psychological level could open a path towards $1,180. |

| Re: FXTM Daily Market Analysis by Forextime: 5:22am On Sep 12, 2018 |

Daily Fundamental ForexTime ( FXTM ) Sterling weakens despite wage growth surprise  There was appetite for the British Pound on Tuesday morning following official data that showed UK wage growth accelerating faster than expected. However, gains were later surrendered as investors redirected their focus back toward Brexit developments. UK wage growth surprised to the upside by rising 2.9% in the three months to July while the unemployment rate remained steady at 4% - its lowest level since March 1975. Although the jobs report illustrates an encouraging picture of the UK economy, this is unlikely to convince the Bank of England to raise interest rates anytime soon. The central bank is poised to remain on hold until the thick smog of uncertainty created by Brexit fully dissipates. Sterling’s extreme sensitivity to Brexit headlines has clearly become a dominant market theme. The explosive price action witnessed yesterday following encouraging comments from the EU’s chief Brexit negotiator is a testament to this fact. While a renewed sense of optimism over a Brexit deal possibly secured within 6-8 weeks could push Sterling higher, any hiccups during the talks are likely to expose the currency to downside shocks. Looking at the technical picture, the GBPUSD is turning bullish on the daily charts. Prices are trading above the daily 20 Simple Moving Average while the MACD is in the process of crossing to the upside. Bulls will remain in control as long as the GBPUSD is able to keep above the 1.3000 level. However, a breakdown below 1.3000 could inspire a decline back towards 1.2940. Across the Atlantic, the Dollar rebounded against a basket of major currencies as rising global trade tensions boosted its safe-haven demand. The Dollar is likely to remain king across currency markets on the back of US rate hike expectations and the bullish sentiment towards the US economy. Taking a peek at the technical picture, the Dollar Index could challenge 95.80 once bulls are able to secure a solid daily close above 95.50. |

| Re: FXTM Daily Market Analysis by Forextime: 4:54am On Sep 18, 2018 |

Daily Fundamental ForexTime ( FXTM ) Chinese Yuan shows resilience, despite emerging markets pressured by trade concerns  Conflicting indications over the status of trade talks between the United States and China has contributed towards a subdued opening of the week for financial markets. Reports that President Donald Trump will most likely impose tariffs on $200 billion worth of Chinese goods have collided with other reports that Beijing was considering rejecting trade talks with Washington. This collectively resulted in a cautious start to the trading week for investors, where they prefer to remain on the side-lines and await clarity on this ongoing issue before deciding what step to take next with their portfolios. The atmosphere of caution and confusion has been reflected across the emerging market space with equities tumbling 1% while most EM currencies depreciated against the Dollar. The Indian Rupee was a clear casualty of the uncertain external environment as it depreciated roughly 0.90% against the Dollar. It has been a painful year thus for the Rupee which has tumbled 12% against the Dollar (YTD), making it one of the world’s worst performing currencies this year. A heavily depressed Rupee will have significant ramifications on the Indian economy, especially when considering how the nation is a major energy importer. With a depreciating Rupee potentially stoking inflationary pressures, the Reserve Bank of India could be forced to hike interest rates for the third time this year. Elsewhere, the Turkish Lira tumbled roughly 1.96% against the Dollar as concerns resurfaced over President Recep Tayyip Erdogan’s grip on the economy. It seems the “feel good” effect from last week’s bold rate hike by Turkey’s central bank has worn off with traders refocusing on the political and economic developments within the Turkish economy. Investors will be keeping an eye out for the Turkish government’s new medium-term program (MTP) to be announced on Thursday which could provide insight into the direction of Turkish economic policy. The Lira could roar back to life if the (MTP) shows signs of the authorities embracing a tighter fiscal program to support growth. In China, the Yuan fought back against the Dollar despite escalating trade tensions weighing on market sentiment. The Yuan’s resilience could be based on Dollar weakness, or that investors may be directing more of their energy to attacking currencies belonging to markets with high current account deficits. Looking at the technical picture, the USDCNY has the potential to challenge 6.8290 if bears are able to secure a daily close below 6.8500. Gold sparkled in the background as escalating trade tensions supported the flight to safety. A softer Dollar stimulated appetite for the yellow metal further with prices punching above the psychological $1200 level. While Gold could appreciate further in the near term, gains remain threated by key fundamental themes. With the Greenback heavily supported by “safe-haven” demand and the Fed poised to raise interest rates this month, Gold is destined for further pain. King Dollar tumbled into the trading week losing ground against a basket of major currencies despite global trade developments denting investor confidence. There is a possibility that the weakness observed could be on the back profit taking ahead of the possible announcement of additional tariffs on China. Technical traders will continue to closely observe how the Dollar Index behaves above the 94.50 support level. An intraday breakdown below this region could inspire a move towards 94.10. |

| Re: FXTM Daily Market Analysis by Forextime: 10:54am On Sep 21, 2018 |

Daily Fundamental ForexTime ( FXTM ) Could the Dollar be turning the corner?  Currencies throughout Asia have welcomed the news that the Dollar has tumbled to a near 3-month low. A number of different currencies in the region have advanced against the Greenback, with the weakening momentum for the Dollar benefiting the Indian Rupee the most at time of writing. The indications that the market is turning more negative towards the Greenback would represent very positive news for emerging market currencies in particular, which have received a pounding over the past couple of months in response to the prolonged Dollar strength in the market. This can be seen during trading on Friday with the Thai Baht, Chinese Yuan, Philippine Peso, Indonesian Rupiah, Malaysian Ringgit and Indian Rupee all strengthening. The exact catalyst behind why the Dollar is weakening is not easy to point out, but the main contender is that fading fears over trade tensions are providing traders with a reason to take profit on Dollar positions that have been building for months. Another round of reassuring comments from authorities in China indicating that the Chinese Yuan will not be used as a weapon in the trade tensions has also been looked upon positively by the market. It does overall go without saying that the prospects for more potential weakness in the Dollar moving forward would of course be widely welcome news for a long list of currencies across the globe. As we head into the conclusion of trading for the week the South African Rand has benefited the most from weakness in the Greenback. The Rand has strengthened above 4% over the past five days, with traders looking very positively on the news that the South African Reserve Bank (SARB) were able to leave monetary policy unchanged yesterday. The news that inflationary pressures in South Africa unexpectedly eased in August earlier this week allowed the SARB to maintain resilience and not follow the recent path of both the Russian and Turkish central banks to raise interest rates, which was needed in both the cases of Russia and Turkey to ease inflationary pressures and defend both the Ruble and Lira from further weakness. It is not surprising that the Turkish Lira remained volatile and has shifted between both gains and weakness in the aftermath of Turkey’s finance minister announcing his plan to combat the Lira currency crisis. The market as you would expect has looked upon the announcement negatively that there has been a sharp downgrade in GDP growth forecasts for both 2018 and 2019. Growth is now expected to slow below 4% this year and narrowly above 2% in 2019, which is a sharp contrast to the overall growth at 7.4% that the economy enjoyed last year. I would keep a very close eye on the British Pound over the upcoming sessions despite the news that the Cable has rallied to its highest levels in nearly three months. Traders appear to have repositioned in recent sessions that there will eventually be a breakthrough in the UK and EU negotiations over Brexit, but the latest summit in Salzburg failed to result in a positive outcome and the rally in the Pound can fall like a house of cards if the markets begin to reprice into the market a potential hard-Brexit eventuality. |

| Re: FXTM Daily Market Analysis by Forextime: 4:33am On Sep 27, 2018 |

Daily Fundamental ForexTime ( FXTM ) Dollar steady after Fed raises interest rates  In a widely expected move, the Federal Reserve has raised its key interest rate by 25 basis points for the third time this year. The central bank expressed optimism over the US economy and projected growth to remain at a steady pace through 2019. Inflation was forecast to linger around 2% over the next two years while the unemployment rate seen falling to 3.5% next year. All in all, the relatively upbeat assessment of the US economy and little concern shown over trade tensions reinforced expectations of a rate hike in December. However, the key takeaway was the removal of the word “accommodative” from the statement which was seen as a dovish signal that suggested slower interest rate increases next year. In regards to the technical picture, the Dollar Index briefly depreciated before later clawing back losses as investors digested the updated dot plot and economic projections. The Dollar’s overall reaction to the Fed rate decision and press conference was fairly muted with prices trading around 94.30 as of writing. A breakdown below 94.00 could trigger a decline back towards 93.80. Alternatively, a move above 94.30 may inspire bulls to attack 94.50. |

| Re: FXTM Daily Market Analysis by Forextime: 4:12am On Oct 02, 2018 |

Daily Fundamental ForexTime ( FXTM ) Rescued NAFTA deal revives risk-on sentiment, Yen crumbles  Investors have entered into the final trading quarter with a renewed appetite for risk after Canada agreed to join the United States and Mexico in a trilateral trade deal over the weekend. Global equity markets powered higher on this positive development, while the Canadian Dollar and Mexico peso both soared to fresh multi-month highs. With the new United States-Mexico-Canada Agreement (USMCA) seen as a breath of fresh air to markets, “risk-on” could remain the name of the game in the short term. However, market sentiment remains gripped by ongoing US-China trade tensions in the medium to longer term. Any fresh signs of trade tensions escalating between the world’s two largest economies could dent investor confidence and erode risk appetite. In the currency markets, the Japanese Yen was a clear casualty of the “risk-on” mood with the currency depreciating to levels not seen November 2017. An appreciating Dollar rubbed salt into the wound with the USDJPY trading towards 114.00 as of writing. With investors likely to offload the shun the Japanese Yen for riskier assets and the Dollar supported by rate hike expectations, the USDJPY could trade higher. In regards to the technical picture, a solid daily close above 114.00 could send the USDJPY towards 114.50.  The Canadian Dollar bulls were unstoppable today mostly due to the NAFTA optimism with the USDCAD crashing towards levels not seen in over 4 months below 1.2800. With the CAD heavily supported by higher oil prices and expectations over the Bank of Canada raising interest rates this month, the USDCAD could potentially sink towards 1.2700 and beyond. Investors will continue to closely observe if bears are able to secure a solid weekly close below the 1.2800 level. Gold traded in the background with prices bouncing within a modest range despite investors offloading safe-haven assets for riskier investments. The yellow metal may remain on standby ahead of the US jobs report on Friday. Daily bears remain in control below the $1200 psychological level with $1181 acting as a near-term bearish target.  |

| Re: FXTM Daily Market Analysis by cheezy4real(m): 5:17am On Oct 02, 2018 |

Please reach m on 08037085441. WATSapp or call |

| Re: FXTM Daily Market Analysis by Forextime: 5:11am On Oct 09, 2018 |

Daily Fundamental ForexTime ( FXTM ) Yuan eases on risk-off sentiment, regional currencies suffer and Gold tumbles  Financial markets have entered the new trading week on negative footing as a mixture of different market themes weigh on investor sentiment and promote risk aversion. Ongoing external uncertainties around matters such as trade tensions and the Italian budget coupled with increased optimism over higher US interest rates at a time where questions remain over what will happen to Iranian Oil exports from next month represent just a few of the uncertain themes that are promoting a risk-off atmosphere. The announcement from the PBoC to cut the RRR requirement for the fourth time in 2018 hasn’t been enough to inspire potential buyers back into global stock markets for now. This lack of appetite for risk was reflected across Asian markets, with Chinese equities witnessing heavy losses following a week-long holiday. The Shanghai Composite Index shed 3.7% while the CSI 300 Index plunged 4.3%. With heightened trade tensions denting risk sentiment and the prospects of higher US rates spooking investors, this could be a rough week for global stocks. In the currency markets, the Yuan has weakened to its lowest level in nearly two months against the Dollar on the backdrop of a combination of external and domestic factors. It is possible that the latest move from the PBoC to ease monetary policy by cutting the RRR requirement is a possible driver behind the offshore Yuan weakening as much as 0.5 as the USDCNY advanced back above the 6.90 level, but it is also important to take into account that a resilient Dollar has weighed heavily on a number of different emerging market currencies. The technical picture on the USDCNY is firmly bullish on the daily charts with prices trading marginally below 6.9300 as of writing. A decisive daily close above the 6.9300 level could inspire a move higher towards 6.9347. This increases the likelihood that losses in the Yuan could extend further into the week, which would be something to monitor on a global level due to how correlated Yuan moves can be for regional currencies in the APAC region and specifically because the U.S Treasury repeated previous comments that it is concerned that China is manipulating its currency. The overall risk-off vibe looks to be a threat for investor sentiment into Tuesday, and we do look at risk to suffering from a fragile global marketplace this week. Emerging market currencies stand to be in trouble this week amid risk aversion, prospects of higher US interest rates and Dollar strength. The impacts of the recent spike in US Treasury yields continues to be reflected across most major EM currencies with the Indian Rupee crashing to a new record low past 74.00, the Indonesia Rupiah touching a fresh two-decade low and South African Rand sinking to its lowest level in three weeks. With the pressure across EM likely to mount, especially for those economies with currency account deficits and high levels of debts, the outlook looks gloomy for emerging markets. Across the Atlantic, the Dollar is poised to find support from safe-haven flows, rate hike expectations, and optimism over the strength of the US economy. With the United States firing on all cylinders and the Fed expected to raise rates in December and another three times in 2019, the interest rate differential trade supports the Greenback. In regards to the technical perspective, the Dollar Index may be gearing for further upside on the daily charts with a bull’s steadily eyeing the 96.00 level. A solid close above this point could inspire prices to challenge 96.43 in the near term. A strengthening Dollar has resulted in Gold experiencing its biggest one-day selloff since the middle of August with prices trading marginally below $1185.00 as of writing. The price action in recent weeks continues to highlight how the precious metal remains negatively correlated to the Greenback. With the fundamental drivers behind the Dollar’s appreciation still firmly in place, Gold’s outlook points to further weakness. Sellers need a solid daily close below $1190 to open a smooth path towards $1180 and $1174, respectively. |

| Re: FXTM Daily Market Analysis by Forextime: 4:58am On Oct 12, 2018 |

Daily Fundamental ForexTime ( FXTM ) Yuan firms on Dollar weakness, Risk aversion reigns  Global investors will likely remain on high alert throughout the end of the week to see if the largest market sell-off since early 2018 will continue. It has been an incredibly tense and volatile trading week for financial markets with equities across the globe collapsing on widespread risk aversion. The International Monetary Fund’s (IMF) gloomy global growth forecast and ongoing market uncertainties over external unknowns, such as trade tension are just a handful of the many themes that could be encouraging this sudden nosedive in investor sentiment. The repeated criticism from President Trump in the direction of the Federal Reserve regarding higher US interest rates is only adding to the bucket load of market uncertainty. When you combine all the different elements of financial market risk across all corners together, it becomes no surprise that risk aversion has exploded out of control. While Trump has a part to play in the current stock market selloff, there are other key factors brewing in the background. Global equity bulls are engaged in a fierce battle with rising U.S bond yields, ongoing trade tensions, global growth concerns and the prospects of higher US interest rates. For as long as these themes remain, speculation is likely to heighten over the party coming to an end for stock bulls. This might well mean the long-awaited stock market correction. It has been a bloodbath of market selling across regions throughout the globe. In China, no prisoners with taken with the Shanghai Composite Index plunging 5.22% while Hong Kong stocks shed 3.54%. European equity markets were a sea of red while U.S stocks extended losses with the Dow Jones Industrial Average dropping more than 500 points for a second straight day. In the currency markets, the Chinese Yuan strengthened against the Dollar in line with many other emerging market currencies advancing against the USD. This came in spite of the PBoC setting the midpoint rate lower for the ninth consecutive day and might have been encouraged by weakness in the Greenback after President Trump once again lashed out at the Federal Reserve. A weaker Dollar from this point would be positive for emerging market currencies, but we must also monitor the potential risks that EM currencies could fall victim to the “risk-off” environment and the prospects of higher US interest rates. In regards to the technical picture, the USDCNY will be positioned to test 6.86 if a daily close below 6.90 is achieved. |

| Re: FXTM Daily Market Analysis by Forextime: 10:59am On Oct 29, 2018 |

Daily Fundamental ForexTime ( FXTM ) Equity sell-off resumes in Asia  The steep sell-off in U.S. equity markets suggests October could be the worst month since the global financial crisis of 2008. Seven trillion dollars have already been wiped from the global market cap, and still there are no signs of bulls returning. Chinese stocks fell today with the CSI 300 declining more than 3% while the Yuan remained trading near a decade low. The Nikkei 225 gave up gains of more than 1% to trade in negative territory. Moving against the trend were stocks in Australia, with the ASX 200 gaining more than 1% supported by the healthcare and telecom sectors. The bears seem well in control of the market and there’re many reasons to justify their actions. Whether it’s weakening global economic growth, the ongoing U.S.-China trade war, monetary policy tightening, fears of a hard Brexit, Italy’s budget woes… and the list goes on. What is more interesting is that investors are even punishing companies that have reported positive earnings surprises. To date, almost half of S&P 500 companies have announced earnings results for Q3. Out of 241 companies, 77% managed to beat on EPS, and 59% beat on sales according to FactSet. Companies that have reported positive earnings surprises saw their stocks declining 1.5% on average two days before the earnings release through two days after the announcement. So, earnings do not seem to be a key reason for the market sell-off despite some big names like Amazon and Alphabet disappointing investors. In fact, valuations are becoming attractive following a 10% plunge in the S&P 500. Forward P/E ratio is currently standing at 15.5 compared to the 5-year average of 16.4. That’s the time when investors should consider buying companies with strong fundamentals. This is especially the case when economic data is still supporting. Friday’s data showed the U.S. economy expanded 3.5% in Q3 after 4.2% growth in the previous quarter mainly driven by consumer spending. So far, it seems more of a market correction than signs of a recession. However, if leading economic indicators begin pointing south while the Federal Reserve keeps raising interest rates, the stocks correction may become a bear market. Inflationary pressures are the biggest risk to preventing the Fed from slowing the tightening cycle. That’s why investors need to keep a close eye on Friday’s U.S. wage growth figure. |

| Re: FXTM Daily Market Analysis by Forextime: 6:25am On Nov 06, 2018 |

Daily Fundamental ForexTime ( FXTM ) Conflicting trade signals set the tone; GBP remains way off 1.35 “target” on Brexit deal [IMG]https://pbs.twimg.com/media/DrScykKVAAA7FlH.jpg[/IMG] [SIZE="3"]The early part of trading for the week has already showed how sensitive emerging markets can react to newsflow around potential trade developments with a number of different emerging market currencies trading lower against the USD on Monday. This has included losses close to 1% in the Indian Rupee, while the Chinese Yuan has lost just over 0.5% and the Malaysian Ringgit above 0.4%. This trend of trajectory does overall sum up how sensitive emerging market assets will be to newsflow around a potential breakthrough in trade talks between the two largest economies in the world. [B]Air of caution before U.S. risk events this week[/B] Elsewhere, there are some indications at time of writing of limited trading volumes as the new trading week commences, which sum up that investors could be hesitant to add more positions into their portfolios just one day before mid-term elections take place in the United States. When you consider how off-guard financial markets have been caught to political events in recent history, caution before the event is a likely investment strategy that is on the mind of investors. This means that we might not see much movement in global stocks before the event, while safe-haven assets like Gold and the Japanese Yen will be the first thing on traders’ minds if an air of market uncertainty comes their way. The general consensus is that while, overall, mid-term elections do not on a historic basis create too much fuss in financial markets, this administration running the White House is unlike anything we have seen before and this is why it is expected that investors will tread with caution before the outcome becomes clearer. It is not possible to predict potential political outcomes in the modern world of unpredictable politics, but most emerging market investors will be hoping the Dollar does sell-off on the outcome of the election because emerging markets do appear heavily undervalued at current levels. The upcoming Federal Reserve meeting will be another risk event to monitor this week, but interest rates are not expected to change in November and as long as the FOMC carries the same narrative that U.S. interest rates will be gradually adjusted higher in the next 15 months or so, the mid-term elections should overshadow the Fed decision when it comes to potential financial market volatility. The best-case scenario for investors who would like to consider selling the Dollar at what still appears to be historically-high valuations for the Greenback would most likely be that the mid-term election outcome encourages concerns that President Trump will face legislative resistance when it comes to pushing pro-America policies. Emerging markets are those that remain greatly pressured from broad-based Dollar strength, so I would expect emerging market currencies to be contenders to benefit the most over the medium-term if the Dollar does get squeezed lower. [B]Sanctions were re-imposed into Oil price long time ago[/B] The return of re-imposed sanctions on Iran on November 5 has encouraged a small recovery in the Oil markets today. However, I wouldn’t buy into this headline too much, because we could be in line for a small recovery in the Oil markets after the commodity edged dangerously close to bear market territory after withdrawing close to 20% from its multi-year highs a few weeks ago. Re-imposed sanctions on Iran have been something that were priced into the Oil markets a long time ago, all the way back from when Trump confirmed he would pull out of the 2015 nuclear deal, so I wouldn’t associate sanctions coming back into play as a near-term driver for the price of Oil. I would instead, focus more heavily on the global demand outlook because of the ongoing external uncertainties weighing down on economic prospects. This is something I see of more of a risk for Oil over the coming months. If concerns over slowing global growth come to fruition, it signals less demand is needed for commodities like Oil and I see this as a major risk to the valuation of Oil. [B]Hopes of Pound rising above 1.35 on Brexit deal long way off![/B] Optimism that a long-awaited breakthrough on the prolonged Brexit negotiations is close has sent British Pound forecasts into a frenzy. Suggestions are making their way that the Pound could rally all the way to 1.35, if not above on an eventual breakthrough in the Brexit drama, but I would personally stay away from such claims. Yes, we all know how sensitive the British Pound has behaved to Brexit newsflow but let’s not get ahead of ourselves and suggest a return to 1.35 is imminent when the GBPUSD is trading marginally above 1.30 at time of writing. UK Prime Minister Theresa May will still need to receive approval for the terms of the soon-to-be-expected agreement, which given the ongoing controversy that Brexit still receives around the United Kingdom will likely not be an easy task. I would personally factor into consideration that the Pound is just as much likely to shoot lower once again on more Brexit gridlock, as it is to aim higher on a breakthrough. Such headlines on an expected rally in the Pound generally suggest that markets are positioning themselves on a breakthrough, meaning that I would factor into my own expectations how suddenly the Pound could fall sharply below 1.30 on another round of hard-Brexit fears. |

| Re: FXTM Daily Market Analysis by Forextime: 9:56am On Dec 03, 2018 |

Daily Fundamental ForexTime ( FXTM ) Temporary trade truce provides additional boost to risk  Just a few days after Fed Chairman Jerome Powell unexpectedly signaled that the Federal Reserve is turning dovish, investors received further positive news over the weekend after a temporary ceasefire between Washington and Beijing regarding trade tensions was announced after the G-20 summit in Argentina. The two-hour dinner between senior authorities from both the United States and China, including President Trump and President Xi, that led to the announcement of a temporary trade truce was of greater importance than the G-20 communique which stated that the WTO needs to be reformed to improve its function. What was delivered over the dinner was not a breakthrough, neither a long-term solution for the ongoing trade war between the largest two economies, but a 90-day window to improve relations. Introduction of new tariffs are now shelved, and trade talks will intensify over the next three months. This outcome seems to be an optimistic one from the two leaders and more than what was priced into markets beforehand, meaning that this is enough to boost sentiment and risk-on trade. Chinese stocks rose more than 3% and the S&P 500 futures surged 1.7% at the time of writing. While bulls seem to be well in control for now, investors need to know that what was achieved is only a short-term relief to markets. Whether this will be translated into longer-term advances depends on the path of negotiations over the next three months. For now, one obstacle has been removed, but all longer-term risks remain there. Canada joins Saudi Arabia and Russia in managing production The risk-on rally sent Brent Oil above $62 early Monday. The U.S.-China trade truce is not the only source of support for prices, but signals of another production cut from Russia and Saudi Arabia seem to be the key factor. OPEC’s official meeting will be held on Wednesday and markets are expecting to see a substantial production cut after Russian President Vladimir Putin said his country’s cooperation on Oil supplies with Saudi Arabia would continue. Another surprising announcement came from the government of Alberta on Sunday stating a cut of 325,000 barrels a day for three months starting in 2019. Given this combination of factors, Oil prices are likely to have bottomed out for 2018, but a confirmation is needed when OPEC and non-OPEC members meet in Vienna on December 6. Dollar heads south The demand for riskier assets sent the Dollar lower against most developed and emerging market currencies. The Dollar index fell back below 97 with commodity currencies AUD and CAD being the best performing ones. The Chinese Yuan also broke a three-week trading range to trade 0.8% higher against the Greenback. This relief rally may continue for the next couple of days, unless surprising negative news arises. |

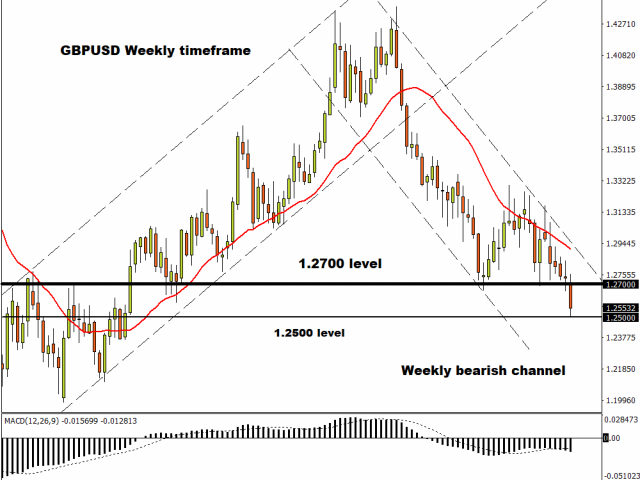

| Re: FXTM Daily Market Analysis by Forextime: 4:07am On Dec 11, 2018 |

Daily Fundamental ForexTime ( FXTM ) EM Currencies hit by risk aversion; Pound dives on delayed Brexit vote  Emerging market currencies are poised to remain in the firing line this week as ongoing trade tensions, Brexit uncertainty, depressed equity markets and turmoil in France cripple investor confidence. The unfavourable market conditions are already boosting appetite for the safe-haven Dollar, which will most likely translate to further pain and punishment for EM currencies. With concerns over plateauing global growth and geopolitical risk leaving sentiment extremely fragile, risk aversion has the potential to become a major theme in the near term. In the currency markets, the Chinese Yuan weakened against the Dollar mostly due to trade tensions. An appreciating Dollar weighed on the local currency further with the USDCNY trading marginally above 6.908 as of writing. With trade tensions seen weighing on the Yuan but strengthening the Dollar, the USDCNY has scope to challenge 6.923 in the near term. Chaos in Commons as May delays Brexit vote The British Pound was treated without mercy by bearish investors on Monday after UK Prime Minister Theresa May abruptly postponed a parliamentary vote on her Brexit deal. Appetite towards Sterling instantly diminished following the news with the GBPUSD crashing to levels not seen since April 2017. A strong sense of uncertainty over the various scenarios that could happen regarding Brexit is likely to leave investors extremely uneasy and edgy. As the week progresses market players will be pondering whether May has the ability to renegotiate with Brussels in a bid to save the deal? If she will face a leadership vote or the possibility of a second referendum. With Brexit chaos in the House of commons raising the likelihood of a no-deal scenario, the near-term outlook for the Pound points to further downside. In regards to the technical picture, the GBPUSD is heavily bearish on the weekly charts. The downside momentum could send prices below 1.2500. Bears remain in firm control below the 1.2700 resistance level.  Currency spotlight – Dollar The Dollar staged an impressive rebound as trade tensions and Brexit related uncertainty sent investors sprinting to the safe-haven currency. Although the Dollar has scope to extend gains on safe-haven flows, the upside is poised to face headwinds in the form of fading Fed hike expectations. With November’s disappointing US jobs report reinforcing expectations over the Federal Reserve taking a pause of rate hikes next year, Dollar bulls are at threat of running of inspiration in the medium term. Focusing on the technical picture, the Dollar Index has scope to hit 97.50 this week. |

{kind=link}

Bread Wrapper/nylon / Finally! How To Rack Up Facebook LIKES In Nigeria / What Bizness Can I Do Or How Do I Make Money Using My Blackberry Phone

(Go Up)

| Sections: politics (1) business autos (1) jobs (1) career education (1) romance computers phones travel sports fashion health religion celebs tv-movies music-radio literature webmasters programming techmarket Links: (1) (2) (3) (4) (5) (6) (7) (8) (9) (10) Nairaland - Copyright © 2005 - 2024 Oluwaseun Osewa. All rights reserved. See How To Advertise. 192 |